All Categories

Featured

:max_bytes(150000):strip_icc()/Pros-and-cons-indexed-universal-life-insurance_final-1b83c0fd52154eb69edd47f99ab8927a.png)

[/image][=video]

[/video]

This can result in less benefit for the insurance holder compared to the monetary gain for the insurance provider and the agent.: The illustrations and assumptions in advertising materials can be misleading, making the plan seem extra eye-catching than it might really be.: Be conscious that financial advisors (or Brokers) gain high compensations on IULs, which might affect their recommendations to sell you a plan that is not appropriate or in your finest passion.

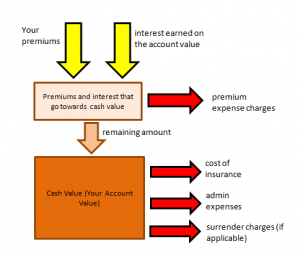

Most account alternatives within IUL items guarantee one of these restricting aspects while enabling the various other to float. The most typical account alternative in IUL policies includes a floating yearly passion cap between 5% and 9% in current market conditions and a guaranteed 100% participation price. The interest made equates to the index return if it is less than the cap however is covered if the index return surpasses the cap rate.

Various other account choices may include a drifting engagement price, such as 50%, without cap, indicating the passion attributed would certainly be half the return of the equity index. A spread account credit histories interest above a floating "spread out rate." If the spread is 6%, the interest credited would be 15% if the index return is 21% however 0% if the index return is 5%.

Rate of interest is generally attributed on an "annual point-to-point" basis, implying the gain in the index is computed from the factor the premium entered the account to specifically one year later. All caps and participation prices are after that applied, and the resulting rate of interest is attributed to the policy. These prices are readjusted every year and utilized as the basis for computing gains for the following year.

The insurance company purchases from an investment financial institution the right to "buy the index" if it goes beyond a specific level, known as the "strike cost."The carrier might hedge its capped index liability by purchasing a call option at a 0% gain strike price and writing a call alternative at an 8% gain strike cost.

Best Indexed Universal Life Policies

The budget that the insurance policy firm has to purchase choices depends upon the yield from its general account. If the service provider has $1,000 internet premium after reductions and a 3% yield from its general account, it would designate $970.87 to its general account to grow to $1,000 by year's end, utilizing the staying $29.13 to acquire choices.

This is a high return assumption, showing the undervaluation of options on the market. The two largest variables affecting floating cap and involvement rates are the yields on the insurance coverage business's general account and market volatility. Service providers' general accounts mainly contain fixed-income assets such as bonds and mortgages. As yields on these possessions have declined, carriers have had smaller allocate purchasing choices, causing minimized cap and involvement prices.

Service providers commonly illustrate future efficiency based on the historical performance of the index, applying current, non-guaranteed cap and involvement prices as a proxy for future efficiency. This method might not be realistic, as historic projections usually show higher previous rates of interest and think consistent caps and participation prices in spite of diverse market conditions.

A much better approach could be allocating to an uncapped involvement account or a spread account, which entail buying fairly inexpensive choices. These strategies, nonetheless, are much less steady than capped accounts and might call for frequent adjustments by the service provider to mirror market conditions precisely. The narrative that IULs are traditional products supplying equity-like returns is no much longer sustainable.

With realistic assumptions of alternatives returns and a shrinking budget plan for acquiring options, IULs might provide marginally higher returns than traditional ULs but not equity index returns. Potential customers should run pictures at 0.5% over the rate of interest credited to conventional ULs to analyze whether the policy is correctly funded and efficient in providing guaranteed efficiency.

As a trusted partner, we work together with 63 top-rated insurance business, guaranteeing you have accessibility to a varied array of alternatives. Our solutions are totally totally free, and our specialist advisors provide impartial recommendations to aid you locate the very best coverage customized to your demands and budget. Partnering with JRC Insurance policy Team means you get tailored solution, competitive rates, and satisfaction recognizing your monetary future remains in qualified hands.

Pacific Life Iul Reviews

We aided thousands of families with their life insurance needs and we can help you also. Professional assessed by: Cliff is a certified life insurance coverage agent and one of the proprietors of JRC Insurance Group.

In his leisure he takes pleasure in hanging out with family, traveling, and the outdoors.

Variable plans are financed by National Life and dispersed by Equity Services, Inc., Registered Broker/Dealer Affiliate of National Life Insurance Policy Company, One National Life Drive, Montpelier, Vermont 05604. Be sure to ask your economic consultant about the long-lasting treatment insurance policy's functions, benefits and premiums, and whether the insurance coverage is appropriate for you based on your monetary situation and goals. Handicap earnings insurance policy usually gives monthly revenue benefits when you are incapable to work due to a disabling injury or ailment, as specified in the policy.

Cash value grows in an universal life plan with credited interest and reduced insurance policy expenses. 6 Policy benefits are reduced by any outstanding financing or finance rate of interest and/or withdrawals. Rewards, if any, are impacted by policy finances and loan rate of interest. Withdrawals over the expense basis may cause taxed normal income. If the plan lapses, or is surrendered, any kind of superior car loans taken into consideration gain in the policy might go through ordinary revenue tax obligations. This change, subject to the cap price(presently 10.5%)and flooring(presently 4%), might be favorable or adverse based upon the S&P 500 price return index performance. Negative market efficiency can create negative reward modifications which might create reduced total cash money worths than would or else have accumulatedhad the IPF motorcyclist not been chosen. The expense of the IPF biker is currently 2 %with an assured price of 3 %on the IPF section of the plan. Policy lendings versus, or withdrawals of, values designated to the IPF could adversely impact cyclist efficiency. Selection of the IPF might limit using particular dividend choices. You must take into consideration the financial investment goals, dangers, fees and fees of the investment firm very carefully prior to investing. Please call your investment expert or call 888-600-4667 for a prospectus, which contains this and other vital information. Annuities and variable life insurance policy provided by The Guardian Insurance & Annuity Company, Inc.(GIAC ), a Delaware firm. Are you on the market permanently insurance policy? If so, you might be wondering which sort of life insurance policy item is appropriate for you. There are a variety of various sorts of life insurance policy available, each with its very own advantages and drawbacks. Determining which is appropriate for you will depend on a variety of elements, like your life insurance policy objectives, your financial dedicationto paying premiums in a timely manner, your timeline for making contributions, and a lot more. This money value can later be taken out or obtained against *. Significantly, Universal Life Insurance policy plans offer policyholders with a survivor benefit. This survivor benefit builds up with time with each premium paid promptly. Upon the policyholder's death, this survivor benefit will certainly be paid to recipients named in the plan contract. 1Loans, partial abandonments and withdrawals will reduce both the surrender worth and death advantage. Under particular conditions, policy car loans and withdrawals may be subject to income taxes. This details is precise unless the policy is a customized endowment agreement. 2Agreements/riders might be subject to extra costs and limitations. Indexed Universal Life Insurance coverage is developed firstly to supply life insurance policy defense. Taxpayers should seek the recommendations of their own tax obligation and legal advisors regarding any tax and lawful concerns applicable to their specific situations. This is a basic interaction for educational and instructional objectives. The materials and the info are not developed or meant, to be relevant to anybody's individual situations. A fixed indexed global life insurance policy (FIUL)policy is a life insurance policy product that gives you the opportunity, when sufficiently funded, to join the development of the marketplace or an index without straight purchasing the marketplace. At the core, an FIUL is created to give defense for your liked ones in the occasion that you die, but it can likewise give you a wide selection of advantages while you're still living. The key differences in between an FIUL and a term life insurance policy is the flexibility and the benefits beyond the fatality advantage. A term plan is life insurance that ensures payment of a specified survivor benefit during a specified time period( or term )and a given costs. As soon as that term expires, you have the choice to either renew it for a brand-new term, end or convert it to a premiumcoverage. An FIUL can be utilized as a security internet and is not a replacement for a long-term healthcare strategy. Make certain to consult your financial expert to see what sort of life insurance policy and advantages fit your requirements. A benefit that an FIUL provides is satisfaction. You can relax ensured that if something happens to you, your household and liked ones are cared for. You're not subjecting your hard-earned cash to a volatile market, producing on your own a tax-deferred property that has integrated defense. Historically, our business was a term provider and we're dedicated to offering that company yet we've adapted and re-focused to fit the altering needs of clients and the requirements of the market. It's a market we have actually been devoted to. We have actually dedicated sources to creating some of our FIULs, and we have a concentrated initiative on being able to provide solid options to customers. FIULs are the fastest growing section of the life insurance policy market. It's an area that's expanding, and we're going to maintain at it. On the various other hand, a It provides tax benefits and usually company matching payments. As you will certainly discover here, these are not replace items and are matched for special needs and objectives. The majority of everyone requires to develop financial savings for retired life, and the demand permanently insurance will certainly depend upon your objectives and economic situation. Contributions to a 401(k) can be made with either pre or post tax obligation bucks(via Roth if your strategy enables). Cash then can expand taxdeferredup until withdrawal during retirement, or when it comes to Roth contributions, taxfree, incomes and all. Further, most companies give a matching payment that the worker would certainly not or else get unless they take part in their 401(k)strategy.

{kind=link}

Latest Posts

Universal Life Insurance

Whole Life Insurance Vs Indexed Universal Life

Index Universal Life Insurance Nationwide